President Trump’s return to office and his determined attempt to fundamentally restructure the US’s global trading relations has ushered in a period of heightened volatility for global markets. Investors are asking questions today that they may not have considered previously, including what level of exposure they want to maintain to the US, and whether or not they are satisfied with ‘global’ allocations that heavily overweight the US market.

What do these developments mean for Japan and Japanese equities?

As a Japan equity specialist, Sumitomo Mitsui DS Asset Management (SMDAM) are pleased to lead the discussion of how Trump’s tariffs are likely to impact the Japanese economy.

SMDAM recently invited clients and external partners to join us for an interactive online session where two of SMDAM’s experts shared their insights into the prospects for the Japanese market looking forward.

Masayuki Kichikawa, Chief Macro Strategist, opened proceedings by talking to the macroeconomic situation in Japan today, before handing over to Alex Hart, Japan Equity Product Specialist, who delved into the internal market dynamics at play today. Alex ended by raising several areas of opportunity identifiable within the Japanese market today, before a Q&A session where both speakers faced questions for the audience.

Where was the Japanese economy before Trump’s tariffs?

As underlined by Masayuki, the Japanese economy was fundamentally well positioned prior to the eruption of volatility. This means that while growth projections have been revised down, the Japanese economy is still projected to grow across FY2025. With recession seen as an unlikely scenario, the positive trends previously observed in the Japanese economy can be expected to cushion the impact of tariffs. SMDAM’s economists have commented at length on these tailwinds to the Japanese market elsewhere.

They can be summarized briefly as below:

- Return of inflation, and with it the ongoing ‘normalization’ of Japanese monetary conditions;

- The steady and gentle revaluation of the Yen;

- Sustainable wage increases for Japanese workers; and

- Continuing progress in the reform agenda targeting Japanese corporate governance.

For these reasons, the downward revision of Japanese growth estimates needs to be seen in context. Japan in Q1 2025 is looking broadly healthy from a macroeconomic point of view, and therefore should be able to adapt to the external shock without dipping into recession.

How has the picture changed?

With the positive context above in mind, however, both speakers sought to emphasize the relatively exposed position of Japan’s large and export-oriented automotive manufacturing sector. SMDAM’s baseline assumption is that the 25% tariff on this strategically important sector is likely to remain in force, and both speakers expounded their views on how this will impact the sector and the wider economy.

In terms of non-automative exports, on the other hand, SMDAM’s view is that the effective tariff rate is likely to be gradually negotiated down from the headline rate of 24% officially announced on President Trump’s ‘Liberation Day’. Our economists see Japan as well positioned to negotiate with the US administration on this, and indeed as external participants pointed out in the Q&A, Japan’s trade negotiation team is reputedly already on the ground in Washington.

How big a shock is expected from the tariffs?

SMDAM’s economic research unit conceptualize the magnitude of the external shock by integrating Japan’s exports to the US as a percentage of GDP with a number of additional variables: the anticipated change in tariff rates, the estimated price elasticity of demand for these exports, a forecasted multiplier, and possible mitigating affects from any fiscal stimulus and potential changes in oil and energy prices.

Drawing all this together, SMDAM are forecasting a negative impact of circa 50bps on GDP growth, with the required proviso that this is based on current information and current expectations of what has already proved to be a fluid and fast-moving situation.

s Masayuki ended by stating in response to the chart below, if the Japanese nominal growth trajectory remains positive – albeit below the previously forecast 2.5% level indicated on the chart below – there would still be considerable room for the TOPIX to experience an upwards movement in response to the positive nominal GDP growth expected for FY2025.

Risk warnings: Past performance is not a reliable indicator of future performance and may not be repeated. An investment’s value and the income deriving from it may fall, as well as rise, due to market fluctuations. Investors may not get back the amount originally invested. This information contains forecasts, such forecasts are not a reliable indicator of future performance.

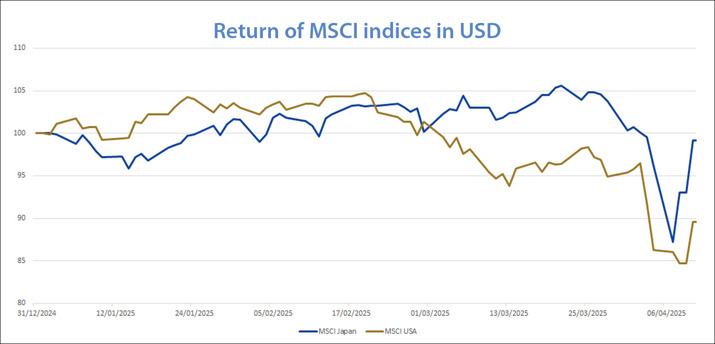

How has the Japanese market performed year-to-date?

Turning to the Japanese market’s internal dynamics which Alex focused on, MSCI Japan has comfortably outperformed MSCI USA in terms of both experiencing a smaller year-to-date drawdown and displaying a quicker and steeper rebound.

Source: Bloomberg as at close 2025/4/10 100 = 2024/12/31

Risk warnings: Performance is shown in USD, the return may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future performance and may not be repeated. An investment’s value and the income deriving from it may fall, as well as rise, due to market fluctuations. Investors may not get back the amount originally invested.

This is partly indicative of the fact that valuations in Japan were already low going into this period of volatility relative to the US, thus serving to cushion the impact of the tariff shock, and also suggests that investors remain confident in the long-term growth potential of the Japanese market.

Alex continued by pointing out part of the cause of the stronger rebound for the Japanese market versus the US has been the strengthening yen. In fact, in yen terms the TOPIX is actually 16% down from it’s previous all-time high of July 2024. The fact that this previous peak is much further back than those achieved by US and other developed market indices shows that Japanese valuations have been hit relatively harder, and as such can be considered to have already adjusted to the tariff shock and are therefore potentially positioned to continue to rebound strongly. For comparison purposes, Alex pointed out that the DAX is down about 12%, and the FTSE 100 by around 10%, from their respective previous peaks.

Our view is that this suggests an unfounded level of pessimism in Japan relative to other developed markets, and this is creating the right conditions for opportunities to emerge. Most tellingly in this respect, the Chinese CSI 300 is down around 12% from its 2024 highs, despite China’s self-evidently greater exposure to US protectionism.

Value vs growth

Going a bit deeper into the style and market-cap dynamics at play, Alex analyzed why value has outperformed growth year-to-date, and touched on why the returns of large- and smid-cap stocks may be set to diverge further under the differentiated influence of the tariffs. Traditionally, small- and mid-cap companies are likely to be more reliant on domestic sources of revenue, and therefore potentially less immediately at risk from trade barriers.

However, Alex carefully explained why this top-down view needs to be supplemented with detailed security-level analysis. With the unintended consequences of Trump’s tariffs set to ripple through global supply chains for some time to come, even companies who appear to be domestically focused could find they are exposed to higher costs eroding their profit margins.

This is one reason why SMDAM’s deep and well-resourced Japan equity research platform is such an essential resource for our portfolio managers to draw upon. Japan is a market where the top-down view always needs to be complimented by the added colour only available from a robust ‘boots-on-the-ground’ analyst presence.

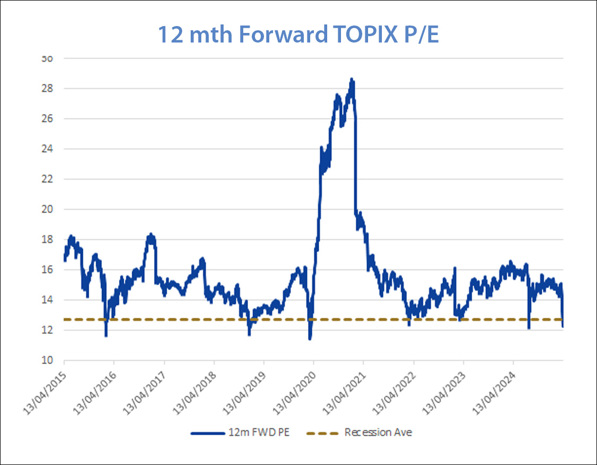

Japan’s valuation ‘advantage’

Japan’s abundance of strong companies trading on comparatively low valuations is not new news; neither is the fact that today this situation may be changing. With the TOPIX already trading on a depressed forward P/E ratio in comparison to the US, the market turmoil of recent weeks has seen this valuation ‘advantage’ expand further. For the macroeconomic reasons discussed in depth by Masayuki, the SMDAM view is that previously attractive valuations have simply become more attractive following these declines.

Risk warnings: Past performance is not a reliable indicator of future performance and may not be repeated. An investment’s value and the income deriving from it may fall, as well as rise, due to market fluctuations. Investors may not get back the amount originally invested.

Reasons to be cheerful

Alex ended with a detailed analysis of winners and losers since ‘Liberation Day’. The role of defensive sectors that have held up well was mentioned, as was the potential over-selling of financials, which may have already created a buying opportunity if SMDAM’s view that recession is unlikely proves accurate.

To highlight to significance of active, bottom-up stock picking in today’s extraordinary context, Alex outlined SMDAM’s view of where pockets of opportunity are already emerging. He focused on companies with strong IP allowing them to monetize the results of their internal R&D. He pointed out that such companies are often able to avoid tariffs through their greater exposure to service and non-tangible exports, and reinforced that pricing power would likely come to the fore as a key variable determining success in the months ahead.

Those firms able to have some control of their final sales price will stand out next to outwardly similar competitors unable to enjoy this privilege. Once again, a key message communicated was that active stock-picking would likely be the best means to unlock the opportunities emerging from today’s volatility.

About the webinar

Join us to hear from our experts on what US tariffs mean for Japan. Please note, the webinar will last 45 minutes and it will be recorded for those unable to attend.

Meet the speakers

Details

Date:

Monday 14th April 2025

Time:

• 09:30 BST (UK Time)

• 10:30 CET (Central European Time)

• 16:30 HKT (Hong Kong Time)

Location:

Live Zoom Webinar

Invest with us

If you have any account or dealing enquiries, please contact BBH using the following contact details:

Brown Brothers Harriman (Luxembourg) S.C.A.

80, route d’Esch, L-1470 Luxembourg

T: +352 474 066 226

F: +352 474 066 401

E: Lux.BBH.Transfer.Agent@BBH.com

Source: SMDAM